Maria Margaronis

June 27, 2011

The Greek verb agorevo means “I speak in public.” But agora also is the market. The market was an area of politics. When you try to separate the two, as neoliberalism does, trying to create a purely economic market place, then there is no democratic control. —George Papandreou, Interview with Open Democracy, 2004

Are we the prodigal children of a neat global economy and an all-successful Europe? Or was the system ailing since its youth? —from Debtocracy, a Greek documentary

Athens—When he was elected prime minister in 2009 at the head of Greece’s Panhellenic Socialist Movement (PaSoK), George Papandreou was going to wipe out corruption, open up politics, rejuvenate the country’s sclerotic economy. “There is money,” he said then, although he must have known there wasn’t any in the public coffers. Less than two years later, he has allowed the “troika” of the European Commission, the European Central Bank (ECB) and the International Monetary Fund to bind him on the horns of an impossible dilemma: either the Greek government implements a second round of austerity measures more savage than any yet endured by a developed country, with deeper cuts and tax hikes and a wholesale, cut-price sell-off of its public assets, or Greece faces default on its sovereign debt, imminent bankruptcy.

Meanwhile, since the end of May, Syntagma Square has overflowed with Greece’s aganaktismenoi (cousins of the indignados who filled Spanish squares this spring), here to refuse the troika’s blackmail and demand their democracy back. On the street in front of Parliament, protesters are banging drums, chanting and waving, singing. The crowd is huge, politically diverse and overwhelmingly peaceful. There are people here from all walks of Greek society; at times the rhetoric is that of a national resistance. A neat elderly couple on their first demonstration push through the crush because their pensions have been slashed, prices are rising and they just can’t make ends meet. Vassilis Papadopoulos, a 50-year-old unemployed truck driver living on loans from his mother, has come all the way from Corinth wrapped in a giant Greek flag, with a look of despair in his eyes and saucepans to bang together. This is a movement, he says, against the political system: “They’ve all cheated us. They destroyed the banks, our pension funds. They invested our social security money in bonds for their own benefit.” Farther down, in the square itself, something entirely new seems to be taking shape. A tent village has sprung up, a liberated zone in which an open conversation has been going on for weeks. University professors, passers-by, unemployed labourers, all get their three minutes with the microphone. There’s a medical tent, a “time bank,” a “team to promote calm.” When riot police cleared the square with clubs on the night of June 15, these protesters didn’t fight. They simply walked right back, picked up the rubbish and repaired their neighbourhood.

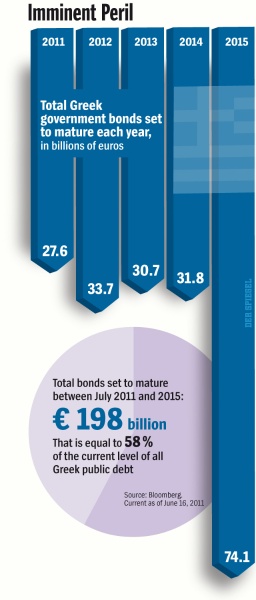

The Greek debt crisis is said to threaten the survival of the eurozone and a global financial meltdown worse than the one set off by the collapse of Lehman Brothers in 2008; each new prediction of default sends frissons of panic and flurries of speculation through the markets. In June the ratings agencies said that German Chancellor Angela Merkel’s plan to persuade Greece’s private creditors to roll over the debt into longer-maturing bonds would be deemed a “credit event”—finance-speak for a default that triggers debt insurance policies, in which American as well as European banks are heavily implicated. That, Merkel told the German Parliament, could have “uncontrollable consequences” for financial markets. At the eleventh hour, an EU summit agreed in principle to a new rescue package of up to 120 billion Euros, but demanded further cuts and tax hikes to close a 5.5 billion euro “black hole” in the existing plan. The markets rebounded. But Papandreou now has to push the new, augmented austerity package through a resistant Parliament before Greece can get the final tranche of last year’s 110 billion euro loan. Without it, the country will be broke by mid-July. The vote is due to take place on Wednesday; Greece's trade unions have scheduled a two-day general strike, and rallies are planned in sixty-five different towns. The Syntagma protesters intend to encircle Parliament.

Already parts of Athens look like New York City circa 1980, with shut-up shops, derelict buildings and graffitied walls. The effects of the game of chicken being played out by bankers and politicians are visible in the way Athenians walk now, head down and defended, through once-safe neighbourhoods; in the irritable, shamed anxiety you see on people’s faces. Depression is endemic; suicide rates have soared. For Greeks, this is much more than an economic crisis. It is a social and political convulsion unlike anything seen here at least since the fall of the colonels’ dictatorship in 1974.

* * *

At a church-run soup kitchen in a dusty park, with his white hair combed back and his clean shirt neatly buttoned, Takis Karis is eating beans from a take-out container. When I ask what brought him here, a furious despair bursts through his gentlemanly manner: “We come so we won’t be hungry. Otherwise, we may as well kill ourselves.” Karis owned a factory, but his business went bankrupt; now he sleeps in the last of the company vans. He has lost his family and, he feels, his country. “You’re speaking to someone who was a Greek, but I’m not a Greek anymore. We’ve given up everything—flag, traditions, family, pride—for money. There is no state, no borders. They brought in 4 million migrants so they could have cheap labour for the Olympic Games and created an unemployment problem.” Niazi, at the same table, joins the conversation in fluent if accented Greek; he came here (legally, he stresses) from Alexandria twenty-seven years ago. He used to make shoes, but then the Chinese arrived and he, too, lost his business. The government, he says, should deport all illegal migrants. “If there is a Europe it has to be for Europeans, not Africans and Asians. An honest man can’t live in Greece anymore. What Greece needs is a new Papadopoulos [the dictator whose junta took over in 1967].” Karis agrees. “Under Papadopoulos, everyone had a job. People would go out and enjoy themselves all night.”

Such rhetoric is not new in Greece, but it’s become more common. A poll in June suggested that 23 percent of Greeks would favour a “strong leader” who could make decisions unencumbered by Parliament; another 31 percent would prefer the country to be managed by a “team of experts.” These numbers reflect the widespread (and not inaccurate) view that a political class steeped in cronyism and corruption has run the country aground and plundered the public purse; hence the cries of “Thieves!” that ring out nightly in Syntagma Square. But they also reflect something more dangerous: a sense of powerlessness, resentment and humiliation that finds no foothold in democracy, reaching instead for scapegoats and too-easy answers.

Athens is living through a double nightmare. Unemployment in Greece is officially at 16 percent, up by 40 percent in a year— 42 percent among the young. Those with jobs face wage cuts of up to 30 percent, tax and price increases, public services in chaos. The social fabric is tearing. Father Andreas, the young priest running the soup kitchen, calls the situation “desperate,” as more and more families find they can’t support their own. At the same time, there is an uncontainable migration crisis. Tens of thousands of Afghans, Iraqis, Pakistanis, Bengalis, Somalis and North Africans are packed into crumbling buildings owned by slumlords, mostly Greek, who double as traffickers. Around Omonia Square, migrants search in rubbish for bottles, cables, clothing, anything to sell. The charity Médecins du Monde has declared a humanitarian emergency; in the lobby of its small clinic young men wait for hours, three deep against the wall.

Like the debt, the migration crisis has a European dimension. Greece is a main entry point for people trying to reach the EU from the Middle East, South Asia and Africa; 150,000 entered the country without papers in 2010 alone. Most of them cross the Turkish border, where the government plans to build a seven-mile wall; hundreds are detained there in conditions unfit for animals. Few want to stay in Greece, but under pressure from the EU the government has tightened controls over the exit points, turning the country into a giant lobster trap to keep migrants from reaching London, Paris or Berlin. According to the 2008 Dublin II Regulation, refugees have to apply for asylum in the first EU country they reach; Greece has 54,000 pending asylum applications and an approval rate of 0.3 percent.

With mass irregular migration and immiseration comes crime, both petty and organized, run by Greeks as well as foreigners. Athens was once seen as Europe’s safest capital; last year there were 145 armed robberies in a single week. The city has become a Mecca for illegal weapons: you can get a “used” Beretta for around 800 Euros or a .357 Magnum for a mere 500. Racist violence is on the rise, as are revenge killings and turf wars. Five dismembered brown-skinned bodies have been found since Christmas at one municipal dump. Even at midday, formerly prosperous streets are lined with women in hot pants and high heels, most of them African; their pimps stay in the shadows. Heroin is cheaper here than anywhere else in Europe.

As the authorities abdicate from policing parts of the city, the task of “keeping order” is assumed by vigilantes affiliated with the neofascist party Chrysi Avgi, or Golden Dawn, which last year won its first seat on the City Council. Chrysi Avgi patrols large areas of Athens, with the explicit or tacit support of many Greek residents and often of the police, staging pogroms against migrants and pitched battles with bands of anarchists who oppose them; on May 19 more than 200 people rampaged through the centre, smashing shop windows and kicking or beating every dark-skinned man they saw while the police stood by. A young sympathizer described the group’s activities to me, proudly lifting his shirt to show a scar on his back inflicted, he said, by an Afghan with a knife. “We go into the basements where they have illegal mosques to check their papers, clear them out. They could be Al Qaeda; they could be anything. It’s not chance that they’re Muslims; they’re coming on purpose to undermine the country. There’s a plan, a secret funding mechanism, and there’s no state to protect us. The police are on the side of the migrants. We had to liberate Attica Square with our fists. The migrants were washing their clothes, their children, in the fountain; they were sleeping and praying in the square. It offends me to see them praying in the square.” This spring a 21-year-old Bengali was stabbed to death in “revenge” for the murder of a Greek expectant father knifed on the street for his camera. Two Afghans have been charged with the killing of the Greek; no one has been arrested for the Bengali’s murder.

* * *

Victoria Square, a stone’s throw from the National Archaeological Museum, used to be a cheerful place full of outdoor cafes; now it contains a few uncomfortable metal seats and ugly concrete planters, “improvements” made for the 2004 Olympics. On a June evening, groups of Middle Eastern men stood talking among themselves; a few women and children sat quietly on the ground. As night fell policemen on six motorbikes roared round and round among them, revving their engines threateningly until most had scattered. Marina Vichou, a third-generation resident and member of a local community group, says that in the past two or three years the area has become “a warehouse for human souls.” Eleni Zoi, who has lived here since 1967, described brothels and gambling dens, illegal shops and filthy apartments where fifty people live without sanitation, filling the airshafts with used toilet paper. “Uneducated people blame the migrants, not the people who rent to them, who are often Chrysi Avgi supporters, or the authorities that fail to integrate them. We kept asking the authorities to do something about the situation, and they wouldn’t—as if they wanted the area to become a ghetto.”

The group came together two years ago, opposing a plan to turn a rare green space into a parking lot; much of their energy is now spent trying to defend the neighbourhood from Chrysi Avgi. “The best way to fight the fascists,” Vichou says, “is to be united and do community things together. It’s very important for people to see that fascist activities are closely connected with illegal ones.” But she feels the cause is hopeless: “It’s all older people here, Albanian immigrants who are not yet established, small shop owners. Chrysi Avgi takes over and won’t allow anyone else to speak. They harass us too, call us filthy names in the street. If I could, I would sell my house and leave.” Zoi—a veteran of many protests, including the occupation of the National Technical University, which helped to bring down the colonels in 1974—insists she won’t be moved. But, she says, it’s the anarchists from a local squat who have so far held the line against Chrysi Avgi. “What can we do? Look at us. We can’t fight them with our fists. I’ve been on countless demonstrations in my life, always peacefully. I’m the one who goes up to people and tells them not to throw things. This is the first time I’ve ever been afraid.”

After decades of expecting everything to be done for them by the state, more and more Greeks are discovering the satisfaction of doing things for themselves: the Atenistas, a network that plants empty lots and cleans up derelict buildings; the community group that filled Kalliga Square with candles when a migrant was murdered there; the cyclists who swoop through the streets in a great flock every week; the campers in Syntagma. But they are working in the shadow of a tidal wave.

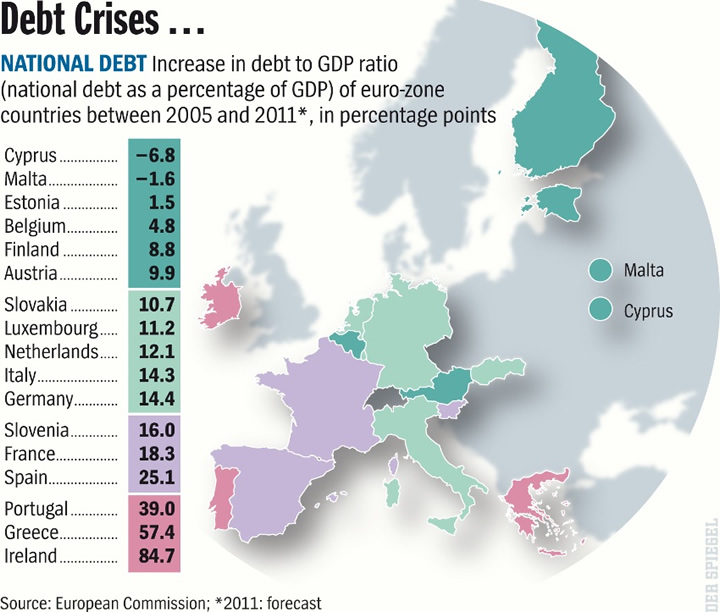

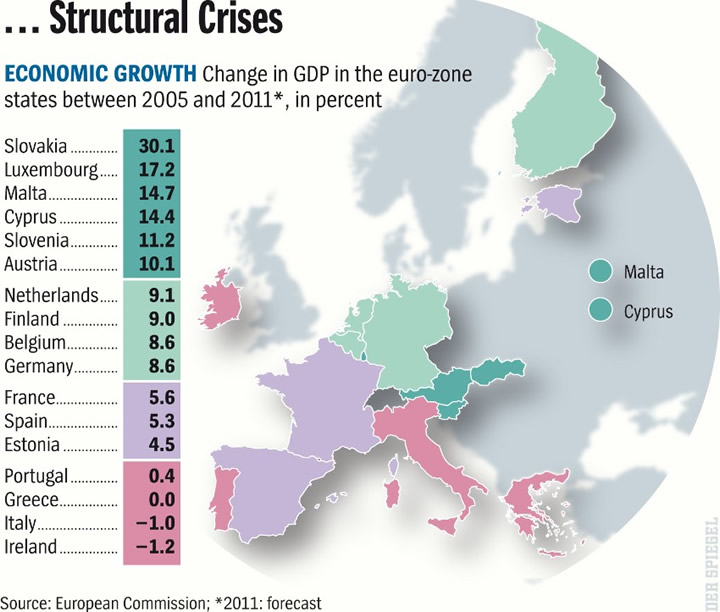

In 2010 Greece’s economy shrank by 4.5 percent; a further slump of 3.8 percent is projected for this year. By the troika’s own figures, even if the Greeks can be forced to accept a second wave of cuts and privatizations, by next year sovereign debt will have risen to 166 percent of GDP; 8–9 percent of GDP will go just to pay the interest. (The interest on US debt, which so exercises Washington politicians, was at 1.3 percent of GDP in 2010.) The country will still be bankrupt, and the drumbeat for default is becoming deafening. What, then, is the point of punishing Greece further?

Despite the contemptuous grumblings of Northern Europeans, Greeks are quick to acknowledge the country’s responsibility for its fiscal mess, sometimes to the point of masochism. (“We ate it together, we’ll pay for it together,” the politicians frown. “We didn’t eat it, you did,” the protesters roar back, pointing to multimillion-euro bribes paid to fixers and legislators by companies like Johnson & Johnson, Siemens and Ferrostaal.) Many Greek intellectuals supported the government’s first agreement with the troika, because it was preferable to disorderly default and because some of its reforms (clamping down on corruption and tax evasion, shrinking the public sector, opening up restricted professions, making it easier for businesses to invest and thrive) have long been necessary but are blocked by vested interests. But such changes can’t be effected in the space of months, in the midst of a deep recession and without democratic control; even economists who backed the plan agree that it had little provision for growth and less regard for Greek realities. Rather than commit hara-kiri by alienating its base in corrupt public sector unions, PaSoK has shut its eyes and slashed the knife across the board, without planning or forethought. Hit by rising taxes and shrinking demand, 50,000 businesses have gone bust in a year. The new austerity package will see most of the state’s assets, from ports to power plants and banks to motorways, sold off to foreign companies, which will have no compunction about firing workers. The troika’s main aim is to rescue not the Greek economy but the country’s creditors—or at least to postpone default until “contagion” can be limited and the banks protected, by transferring the debt to taxpayer-funded lenders like the IMF and ECB.

Since the pain is almost certainly going to get worse, why not simply cut and run back to the drachma, as some of the Syntagma protesters advocate? At least then Greece would be in charge of its own destiny, free to take the traditional route out of debt through devaluation. Some analysts compare Greece’s plight to Argentina’s in 2001, when it saw daylight by unpegging its peso from the dollar. But Greece is not Argentina—among other things, the only oil it produces comes from olives—and even if leaving the euro were possible, the unpredictable consequences could be devastating: economic collapse, rampant inflation, rising nationalism. And while drowning by sudden default may seem a shorter, sharper torment than suffocation by the EU and IMF, the truth is that neither should be necessary.

Although most European bankers and politicians officially shudder at the prospect of a Greek defection from the euro, there are many on the right who would welcome such a “catharsis,” for reasons that Boris Johnson, London’s Conservative mayor, recently explained: “Bit by bit we seem to be creating a fiscal as well as a monetary union, in which huge sums…are being transferred from the richer to the poorer parts of the EU.” The Greek crisis has forced a recognition that the eurozone can’t continue as it is. It must either fly apart under the centrifugal force of the periphery’s debt or become more integrated, a union in which nations have common interests as well as a common currency. Neither option appeals to the bankers and eurocrats—or indeed to the voters of Germany, Britain, France or Finland, the main audience for the spectacle of Greece’s humiliation.

Just as the migrants have become the scapegoat for the Greek people’s suffering, so Greece has become the scapegoat for the structural problems of the eurozone, as well as for the failures of neoliberal orthodoxy. If the medicine isn’t working, it must be the patient’s fault. Greece’s entire economy is worth less than 3 percent of the euro zone's GDP; the obstacles to a more humane, realistic and lasting reform are not financial but political. Like any homeless person on the street in Athens, the country has reached this point for reasons that are particular aa well as systemic. Beginning from the premise that it is in no one’s interest for Greece to default, any lasting solution must address both aspects—which means a rethinking of the euro zone's policies and purposes, and a decision by political leaders to reclaim democratic control from the markets and ratings agencies. It would be pretty to think that such a thing might happen, but no one I know in Athens is holding their breath.

Maria Margaronis June 27, 2011

Related Content

Europe by, and for, Itself

Letters

Europe's Unwelcome Guests

Europe Talks Back

Greek Drama

About the Author

Maria Margaronis writes from The Nation's London bureau. Her work has appeared in many other publications, including the Guardian, the London Review of Books, the Times Literary Supplement andGrand Street.

Talking Tory Blues (Politics, World)

The British election has produced a surprise constitutional earthquake.

D.D. Guttenplan and Maria Margaronis

A Tea Party for Europe? (Racism and Discrimination, Religion, Regions and Countries)

The more Europe's conservatives woo far-right groups, the likelier they are to learn to play nicely together.

Related Topics

Bankruptcy Person Attributes Religion Social Issues Technology War

![The [Greek] European Tragedy](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEiWKI5s90SFm1wWTk6bs4p7CgslaC2SnYPsrZhb-B-smOufNNCSxCvpBLI9hOB-LsXZjir_PNmEiMk2-E62F3xkg96IoC6QFAaZAnPRTVH340IN9WBRmWJqPkjWlgyRj3zpALp7h6hvA58/s920/GkBack_new.jpg)

Article written by Stephanie Flanders Stephanie Flanders

Article written by Stephanie Flanders Stephanie Flanders